Our Primary Strategic Investments are in MGX Resources Limited

(“MGX”, previously known as Mount Gibson Iron Limited) (ASX:

MGX), Tanami Gold NL (“Tanami Gold”) (ASX: TAM), Metals X

Limited (“Metals X”) (ASX: MLX), Dragon Mining Limited (“Dragon

Mining”) (HKEX: 1712) and Prodigy Gold NL (“Prodigy Gold”) (ASX:

PRX), where APAC Resources owns 38.4%, 46.3%, 23.3%, 24.7% and

30.7% as at 31 December 2025 respectively.

The combined net attributable profits shared from MGX, Tanami

Gold, Metals X, Dragon Mining and Prodigy Gold which are

accounted for as the Group’s associates for 1H FY25/26 was

HK$58,912,000 (1H FY24/25: net attributable loss of

HK$5,508,000).

During the period, APAC Resources’ shareholding in Prodigy Gold

rose from 29.6% as at 30 June 2025 to 30.7% as at 31 December

2025 due to subscription of the entitlement offer by Prodigy

Gold (one new share for every one share held) and underwriting

the shortfall offer at an issue price of A$0.002 per share.

MGX

APAC Resources owns 38.4% of MGX at 31 December 2025. MGX is

undergoing a business transition from an iron ore producer to a

gold developer, with the scheduled end of Koolan Island

operation in 2026 and completed acquisition of 50% interest in

the Central Tanami Gold Project Joint Venture. MGX owns the

Koolan Island mine off the Kimberley coast in the remote

north-west of Western Australia.

Due to a significant rockfall on the eastern footwall of the

main pit at Koolan Island in October 2025, mining was suspended.

The investment required to remediate the mine was not

economically justified, especially noting that mining was

scheduled to conclude around September 2026. For now, the

operations are focused on the monetization of lower grade

stockpiles, with processing and shipping of low-grade material

expected to continue to late in the June quarter of 2026.

MGX generated A$15 million free cash flow in the December

quarter of 2025 with the sales of 798,000 wet metric tonnes

(“wmt”) of iron ore (319,000 wmt of average 62.6% Fe iron ore

and 479,000 wmt of average 49.6% Fe iron ore). For the coming

two quarters, MGX targets to process and ship a further 1

million wmt of low grade (42-45% Fe iron ore) stockpiled

material, followed by a full depletion of the mine stocks.

Sales guidance for the year ending 30 June 2026 (“FY25/26”) was

withdrawn on 24 October 2025. MGX’s cash and investment reserves

was A$497 million at the end of 1H FY25/26, although this

doesn’t include the A$50 million payment made in February 2026

upon acquisition of the Central Tanami Gold Project Joint

Venture. Pro-forma MGX has A$447 million cash and investment

reserves.

The Platts Iron Ore Index 62% CFR China index traded strongly in

1H FY25/26, from mid-US$90s per dry metric tonne (“dmt”) in July

to circa US$108 per dmt in late December 2025. At time of

writing in early February 2026, the price is around US$100 per

dmt. Iron ore prices have been supported by strong Indian and

United states (“U.S.”) steel output, while China, Russia, and

European steel production has declined due to weak economic

growth. Iron ore prices are expected to fluctuate with sentiment

related to China and India’s economy.

Tanami Gold

APAC Resources owns 46.3% of Tanami Gold at 31 December 2025.

Tanami Gold’s principal business activity is gold exploration.

It holds 50% of the Central Tanami Project and has a cash

balance of A$14 million. In May 2021, Tanami Gold entered into a

binding agreement with Northern Star Resources Limited

(“Northern Star”) (ASX: NST) to establish a new 50-50 Joint

Venture covering the Central Tanami Gold Project Joint Venture.

On 3 December 2025, MGX reported that it received approval from

the Foreign Investment Review Board for an acquisition for

Northern Star’s 50% interest in Central Tanami Gold Project

Joint Venture, and the transaction was completed in February

2026.

Metals X

APAC Resources owns 23.3% of Metals X as at 31 December 2025.

Metals X is focused on implementing its life of mine plan at

Renison mine, including the development of the high-grade Area 5

deposit. In the six months ended 31 December 2025, the Renison

mine produced 2,796 tonnes of tin (net 50% basis), down 10%

year-on-year, as September quarter mill throughput was impacted

by operational downtime and equipment failures. However,

production rebounded significantly in the December quarter due

to notably higher grades and recoveries as plant operations were

more stable. Production improved in December quarter by 46%

quarter-on-quarter.

Tin prices have rallied from circa A$34,000 per tonne in early

July 2025 to circa A$48,000 per tonne at the time of writing in

late February 2026. Demand for critical mineral stockpiling,

supply challenges such as Indonesia illegal tin mine shut-downs

and Myanmar shipment delays and speculative trading activities

have all contributed to strong tin prices. We remain comfortable

with the outlook for tin due to the lack of supply growth,

growing demand for tin from the electrification trend, and

growth from semiconductors and energy storage industries.

Dragon Mining

APAC Resources owns 24.7% of Dragon Mining at 31 December 2025.

The principal activity of Dragon Mining is gold exploration,

mining, and processing in the Nordic region. Dragon Mining

operates gold mines and processing facilities in Finland and

Sweden. In Finland, the Vammala Production Centre consists of a

conventional 300,000 tonnes per annum crushing, milling and

flotation plant, the Jokisivu Gold mine, the Orivesi Gold mine

which ceased production in June 2019, and the Kaapelinkulma Gold

mine which ceased production in April 2021, and the Uunimäki

Gold project. Annual production from Dragon Mining is in the

range of 20,000 to 30,000 ounces of gold in concentrate

depending on the grade of ore and gold concentrate feed. In

Sweden, the operation is known as the Svartliden Production

Centre, consisting of a 300,000 tonnes per annum carbon-in leach

processing plant together with the closed Svartliden Gold mine

(mining completed in 2013), and the Fäboliden Gold mine where a

campaign of test-mining was completed in September 2020. On 1

April 2025, Allied Properties Resources Limited (“APRL”), a

wholly-owned subsidiary of APAC Resources, announced a

pre-conditional voluntary cash offer of HK$2.20 per share for

all issued shares of Dragon Mining not owned by APRL and its

concert parties. On 19 May 2025, Wah Cheong Development (B.V.I.)

Limited (“Wah Cheong”), an indirect wholly-owned subsidiary of

Allied Group Limited (a substantial shareholder of APAC

Resources), announced a conditional voluntary cash offer of

HK$2.60 per share for all issued shares of Dragon Mining not

owned by Wah Cheong and its concert parties. On 2 June 2025,

APRL’s offer was withdrawn. On 22 September 2025, Dragon Mining

raised HK$172.8 million via a placement of over 31.6 million

shares at HK$5.61 per share.

Prodigy Gold

APAC Resources owns 30.7% of Prodigy Gold at 31 December 2025.

Prodigy Gold is a gold exploration company listed on the

Australian Securities Exchange. It holds a large footprint of

exploration tenements in the Tanami region in the Northern

Territory, Australia, and a JORC resource of 1.03 million ounces

across its Hyperion, Tregony, Buccaneer and Old Pirate projects.

Some of its tenements are held in joint venture with partners

such as Newmont Corporation (ASX: NEM) and IGO Limited (ASX:

IGO). At the end of December 2025, Prodigy Gold has a cash

balance of A$5.2 million. The focus of Prodigy Gold for 2026

will be exploration on the Tanami North Project area and

continue with its strategy to divest non-core assets.

Financial Assets at Fair Value

through Profit or Loss

Financial assets at fair value through profit or loss comprise

mainly the Group’s Resource Investment. As at 31 December 2025,

within the Resources Investment APAC Resources had significant investment representing 5% or more of the

Group’s total assets in Shougang Fushan Resources Group Limited

(“Shougang Fushan”) (HKEX: 639).

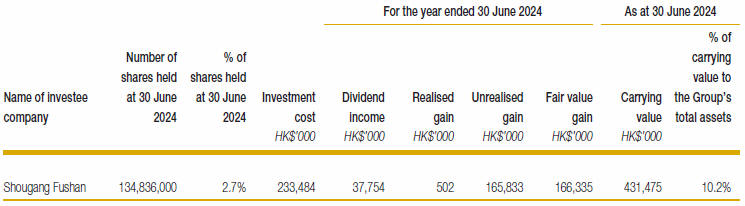

Significant Investment

Our investment in Shougang Fushan generated a fair value gain of

HK$9,985,000 during the period with carrying value as at 31

December 2025 of HK$409,174,000.

Shougang Fushan is a coking coal producer listed on The Stock

Exchange of Hong Kong Limited. Its principal businesses are

coking coal mining and the production and sales of coking coal

products in China. It has three mines located in China with

reserves of 54 million tonnes of raw coking coal at 31 December

2024 and during six months ended 30 June 2025 Shougang Fushan

produced 2.6 million tonnes of raw coking coal and sold 1.6

million tonnes of clean coking coal.

Its results for the year ended 31 December 2025 are not yet

available at the time of writing. The market capitalisation of

Shougang Fushan in early February 2026 is around HK$16.9

billion. During the six months ended 30 June 2025, Shougang

Fushan generated revenue of HK$2,101 million and attributable

profits of HK$481 million and had cash and time deposits of

HK$9.4 billion at 30 June 2025.

Resource Investment

The investments in this segment comprise mostly minor and liquid

holdings in various natural resource companies listed on major

stock exchanges, including Australia, Canada, Hong Kong, the

United Kingdom and the U.S.. Our investments focus on select

commodities within several commodity segments: energy, bulk

commodities, base metals and precious metals.

Resource Investment posted a fair value gain of HK$1,435,886,000

in 1H FY25/26 (1H FY24/25: loss of HK$199,084,000), which, after

accounting for segment-related dividends and other investment

income and expenses, resulted in a segment profit of

HK$1,299,552,000 (1H FY24/25: loss of HK$183,612,000).

Our Resource Investment segment includes, among other investing

strategies, the two resource portfolios announced in August

2016, with an additional natural resource-focused strategy

subsequently established and focused on large caps and

specialist opportunities. The aim of the portfolios is to

produce a positive return using the Company’s funds as well as

to create a track record to attract potential third-party

investments in the future. These various portfolios are managed

under the Resource Investment segment of the Company, which is

separate from the Company’s large strategic stakes. Our

portfolios have a global long-only mandate (cannot short stocks)

and strict parameters on market capitalisation, liquidity,

development stage (exploration through to production) and

jurisdiction to manage risk.

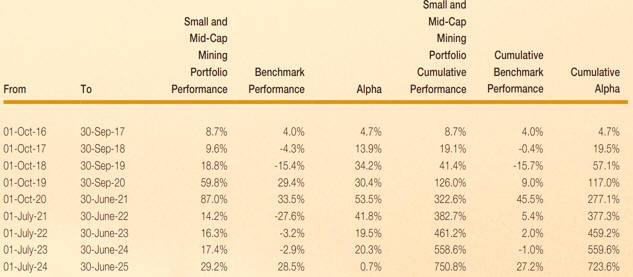

Small and Mid-Cap Mining Portfolio

This portfolio is focused on investments in small and mid-cap

companies involved in the exploration, development and

production of battery metals, base metals, precious metals,

uranium, bulks and other hard rock commodities. Managed by the

same portfolio manager since its inception in October 2016, the

Small and Mid-Cap Mining Portfolio delivered a return of 78.4%

in the six months ended 31 December 2025, which is an

outperformance of 35.0% against its benchmark, which is a

currency adjusted equal weighting of the ASX 200 Small Cap

Resources, FTSE AIM All Share Basic Resources and TSX Venture

Composite indices.

Over its full investment lifetime of October 2016 to December

2025, the portfolio has now delivered a return of 1,418%, which

is a substantial outperformance of 1,335% against its benchmark

return of 82%. A full breakdown of the Small and Mid-Cap Mining

Portfolio’s annual performance against its benchmark is

presented in the table below

The Small and Mid-Cap Mining Portfolio’s exceptional performance

for the six months ended 31 December 2025 was primarily driven

by continued high-conviction positioning in the precious metals

sector. This was supported by a robust macro backdrop for gold

given ongoing central bank buying, the de dollarisation trend,

increasing concerns around fiscal deficits and sovereign debt,

plus significantly higher investor buying (which can be fickle).

The portfolio remains focused on gold producers that are moving

into record margin expansion and cycle-high free cash flows and

this strategy has proved highly effective as investors generally

rerated these companies significantly higher. Consequently, the

list of major contributors was dominated by gold miners,

including Bellevue Gold (ASX: BGL), Equinox Gold (NYSE: EQX), St

Barbara (ASX: SBM), Kingsgate Consolidated (ASX: KCN), Meeka

Metals (ASX: MEK) and Galiano Gold (NYSE: GAU), as well as

Seabridge Gold (NYSE: SA) for leverage to its world class

Kerr-Sulphurets-Mitchell gold-copper development project.

Beyond the precious metals allocation, the portfolio also

benefited from successful stock selection in the critical

minerals space, which has received a surge in investor

attention. Governments globally are increasingly viewing

reliable supply chains through the lens of national security and

are ramping up support for key projects, including fast-track

permitting, grants, direct equity stakes, low-interest loans and

even price floors. The portfolio manager identified this trend

early and held large positions in Q2 Metals (TSX: QTWO) for its

Tier 1 Cisco lithium development project in Quebec, plus EQ

Resources (ASX: EQR), which provides unique leverage to the

global tungsten squeeze via two operating mines in turnaround

under new management.

In contrast to the breadth of positive performers, the portfolio

experienced very few loss-making positions, reflecting the

strength of the underlying commodity environment and disciplined

asset selection. Asante Gold (TSX: ASE) was the only position to

act as a material drag on performance as the portfolio generally

avoided stock specific “banana peels” during the period.

This marks the tenth consecutive period of both positive returns

and outperforming the benchmark. Despite being a long-only

strategy in higher-beta small and mid-cap companies in a highly

cyclical sector, and where the benchmark has recorded five years

of negative returns during those ten years, the portfolio has

never recorded a down year yet.

The lifetime annualised return

is now 34.2%, which compares to the benchmark averaging 6.7% per

year.

Looking ahead, the portfolio manager will continue to

focus on generating alpha by getting the commodity weightings

right via larger positions in high conviction stories that

demonstrate a combination of strong or inflecting free cash

flows, high quality development or exploration potential,

credible leadership, and compelling valuations.

Energy Portfolio

This portfolio is primarily focused on the oil, gas, power and

renewables sectors. At the end of 2019, the mandate for this

portfolio was expanded to include investments in renewables, and

with a broader sector of investments, from February 2020 (before

the full impact of the Covid-19 Pandemic) to January 2026, the

Energy Portfolio has generated a return on investment of 197%.

The investment choices in the Energy Portfolio are selected

through a combination of fundamental bottom up valuation and

analysis of the prospects for different sectors. During the

early days of the Covid-19 pandemic, the investments were

focused in companies in the green energy sector given that the

low interest rate environment was supportive of stocks with

significant growth potential. During 1H FY25/26, we have

continued to focus on companies that support base load power

(predominantly natural gas in certain countries and uranium) and

added select names that were leveraged specifically to the power

demand part of the artificial intelligent (“AI”) Data Centre

thematic. At the same time, we reduced oil exposure

significantly, on the assumption that we would see oversupply

given OPEC+ laid out a path to unwind production cuts. In 1H

FY25/26, oil price fell 7%, although admittedly oil price

performance was not as bad as we initially feared given

restocking demand from the U.S. Strategic Petroleum Reserve,

plus ongoing Chinese purchases as both strategic and commercial

stockpiles continued to grow. The energy transition continues,

particularly in select areas like Energy Storage System. At the

time of writing in February 2026, we are starting to see some

greenshoots in parts of the solar value chain as it appears the

policy overhang is starting to clear up.

Large-Cap Resources Portfolio

This portfolio is strategically focused on high-quality

investments across the broader resources sector, encompassing

leading metals miners and developers, royalty companies,

downstream material producers and physical commodities holding

vehicles. In the six months ended 31 December 2025, the

Large-Cap Resources Portfolio delivered an impressive return of

57.6%, reflecting the powerful tailwinds in the sector during

this period.

The exceptional performance was primarily driven by a strong

allocation to the precious metals sector, underpinned by a

firmly positive outlook on gold and silver (as highlighted in

our Small and Mid-Cap Mining Portfolio section). During the

period, the portfolio focused on high quality gold and silver

developers, where Hycroft Mining (NASDAQ: HYMC) and NovaGold

Resources (NYSE: NG) have been the top contributors of the

portfolio’s performance. Holdings of established precious metals

producers, including Coeur Mining (NYSE: CDE), Equinox Gold

(NYSE: EQX), IAMGOLD (NYSE: IAG), Newmont Corporation (NYSE:

NEM), also contributed to the portfolio’s extraordinary return

in the period.

During the period, there were a few loss-making positions,

including Asante Gold (TSX: ASE) and Allied Gold (TSX: AAUC),

which had experienced volatility driven by risks associated with

operating in less stable jurisdictions such as Ghana and Mali.

However, we see asymmetric risk-reward with the compelling

company valuations, considering the massive cash flow generated

under a resilient gold and silver price environment.

Looking ahead, the portfolio will maintain its emphasis on

sectors experiencing a cyclical upturn, with a selective,

rigorous approach to identifying high quality companies that

offer attractive risk reward profiles. This disciplined strategy

positions the portfolio to continue capitalizing on the

favorable dynamics in resources and precious metals.

Precious Metals

Precious Metals (majority gold exposure) generated a net fair

value gain of HK$1,139,861,000 in 1H FY25/26 (1H FY24/25:

HK$55,082,000). As at 31 December 2025, the carrying value of

the Precious Metals segment was HK$2,110,989,000 (As at 30 June

2025: HK$1,045,084,000). Our largest gold investment in the

Resource Investment segment is in Northern Star (ASX: NST) which

generated a fair value gain of HK$44,123,000 with a carrying

value as at 31 December 2025 of HK$139,310,000. We also own

Westgold Resources (ASX: WGX) which generated a fair value gain

of HK$56,510,000 with a carrying value as at 31 December 2025 of

HK$100,691,000. Northern Star is the largest gold company in

Australia and owns high-grade underground mines in Western

Australia and Alaska. In 1H FY25/26, its production was 728,000

ounces of gold, and it generated a net mine cash flow of A$313

million. In FY25/26, its production target is 1,600,000 -

1,700,000 ounces.

The gold price had a strong rally in 1H FY25/26 from

approximately US$3,300 per ounce and reached a high of US$4,500

per ounce before ending the year at around US$4,300 per ounce.

There is speculation that the strong gold price has been driven

by central bank purchases, safe haven demand amid worries on

geopolitical tensions and expectations that global monetary

policies would loosen.

Bulk Commodities

The Bulk Commodities segment generated a

net fair value gain of HK$47,222,000 in 1H FY25/26 (1H FY24/25:

net loss of HK$128,771,000). As at 31 December 2025, the

carrying value was HK$539,379,000 (As at 30 June 2025:

HK$492,600,000). Our largest investment in this segment during

1H FY25/26 is in Shougang Fushan (HKEX: 639), which generated a

fair value gain of HK$9,985,000 and had a carrying value as at

31 December 2025 of HK$409,174,000.

Base Metals

The Base Metals segment (a mix of copper,

nickel, zinc, aluminium, tin and cobalt companies) delivered a

net fair value gain of HK$88,407,000 in 1H FY25/26 (1H FY24/25:

net loss of HK$21,592,000). As at 31 December 2025, the carrying

value was HK$300,619,000 (As at 30 June 2025: HK$112,239,000).

During the period, base metal prices were strong, with copper

prices up 24.3%, nickel prices up 10.2%, and zinc prices up

12.7%. The Base Metals segment includes our investment in Lundin

Mining Corp (TSX: LUN) which generated a fair value gain of

HK$29,911,000 and had a carrying value as at 31 December 2025 of

HK$58,674,000.

Energy

The Energy segment (mix of oil and gas,

uranium and renewables) had a net fair value gain of

HK$47,444,000 in 1H FY25/26 (1H FY24/25: net loss of

HK$61,989,000). As at 31 December 2025, the carrying value was

HK$232,745,000 (As at 30 June 2025: HK$163,539,000). Our

significant Energy investments include Paladin Energy Limited

(ASX: PDN), which generated a fair value gain of HK$24,778,000

and had a carrying value as at 31 December 2025 of

HK$63,734,000.

Others

We also have a net fair value gain of

HK$114,501,000 from the remaining commodity (diamonds,

manganese, rare earths, lithium and mineral sands among others)

and non commodity investments in 1H FY25/26 (1H FY24/25: net

loss of HK$42,952,000). As at 31 December 2025, the carrying

value was HK$254,863,000 (As at 30 June 2025: HK$113,034,000).

Commodity Business

We have an iron ore offtake at Koolan

Island, and we continue to look for new offtake opportunities

across a range of commodities. For 1H FY25/26, our Commodity

Business generated a segment gain of HK$44,040,000 (1H FY24/25:

loss of HK$6,468,000).

Principal Investment and Financial Services

The Principal Investment and Financial

Services segment, which covers the income generated from loan

receivables and other financial assets. For 1H FY25/26, this

segment recognised a profit of HK$5,732,000 (1H FY24/25: profit

of HK$3,597,000).

Money Lending

Business Model and Customer Profile

The Group provides both secured and unsecured term loans to its

customers under its Principal Investment and Financial Services

segment. Money lending activities diversifies the income stream

and business risks of the Group, and generates a stable return

with the Group’s available financial resources on hand from time

to time. The Group mainly financed its money lending business by

its internal resources.

The Group does not set a specific target for the industry,

business or level of annual revenue to corporate borrowers. The

customers of the Group’s lending business were referred to the

Group through its corporate or business networks. For 1H

FY25/26, customer of the Group’s lending business included a

Hong Kong listed company for an unsecured loan.

Outstanding loan receivables net of loss allowances as at 31

December 2025 amounted to HK$7,298,000 (As at 30 June 2025:

HK$83,578,000). During the period, the Group has written back

impairment losses on its loan receivables of HK$5,683,000 (1H

FY24/25: impairment losses of HK$588,000). Details of a loan

outstanding as at 31 December 2025 are disclosed in note 15 to

the interim condensed consolidated financial information.

Risk Management Policies

The Group adopts a thorough credit assessment and approval

process, and will assess and approve each loan transaction on a

case-by-case basis. The finance department of the Group (the

“Finance Department”) is responsible for conducting a background

check on the prospective borrower in compliance with the

applicable laws and regulations, reviewing the background and

financial strength of such borrower and where applicable, the

guarantor, and enquiring the prospective borrower about the

purpose of the loan and the expected source of funds for loan

repayment. To support its analysis, the Group will obtain

corporate documents, financial statements and search reports of

the borrower and/or the guarantor, and thereafter, assess the

credit risk of the loan and negotiate the terms thereof after

considering (i) the background and financial position of the

borrower or the guarantor (if applicable), including net asset

value and gearing ratio; and (ii) the value of the securities,

if any.

Each loan transaction will be approved by either the Board, or

if the loan principal does not exceed the threshold set by the

Board, by the executive committee of the Board.

The Finance Department monitors the loan and interest repayment

regularly and reviews the annual financial statements of the

borrowers and guarantors (if applicable). It would promptly

report to the chief executive or chief financial officer of the

Group for any delay or default in repayment upon maturity, who

would then formulate plans for loan collection, including but

not limited to requesting for additional securities or

initiating legal actions.

Loan Impairment Policies

The Company adopts expected credit loss allowances (“ECLs”)

according to the requirements of Hong Kong Financial Reporting

Standard 9 issued by the Hong Kong Institute of Certified Public

Accountants. Accordingly, it shall review the recoverable amount

of each loan at the end of each reporting period to ensure that

adequate impairment losses are made. The Group applies a general

approach on loan receivables to assess for the ECLs.

Assessment is done based on the Group’s historical credit loss

experience, adjusted for factors that are specific to the

borrower. In order to measure the ECLs of loan receivables, the

Group will apply a credit rating for each of its borrowers by

reference to each borrower’s past default records, current past

due exposure, an analysis of its current financial position,

likelihood or risk of a default, an assessment on any

significant increase in credit risk, and fair value of

collaterals (if any), and adjust for forward looking information

that is available without undue cost or effort, such as the

current and forecasted global economy and the general economic

conditions of the industry in which the borrower operates.

The Group regularly monitors the effectiveness of the criteria

used to identify whether there has been a significant increase

in credit risk and revises them as appropriate to ensure that

the criteria are capable of identifying any significant increase

in credit risk before the loan amount becomes past due.

Forward Looking Observations

For FY25/26, we remain cautious on the

near-term macro outlook, anticipating a prolonged period of high

market volatility given fluctuations in U.S. trade policies,

geopolitical tensions, fiscal and monetary decisions around the

globe. While the U.S. economy has shown resilience driven by

strong AI investments, the slowing income growth and weak labor

market have driven concern of a gradual turnaround for the

economy’s strength. Mixed economic data points lead to

difficulties in an interest rate cut decision. At the same time,

while China achieved the strong GDP target in 2025, the

sustainability of the growth rate is unclear to us, as a strong

revival in Chinese domestic consumption and property sector is

yet to be seen. We would not discount a potential strong policy

response from the Chinese government to boost the domestic

economy although this doesn’t appear to be a high priority right

now. We believe that precious metals investment demand will

continue to be strong amid the uncertainties around global

economy and rising U.S. debt levels. At the same time, we take a

selective approach on other commodities, which benefit from

structural trends such as energy transition and increasing AI

activity and supportive medium term policies changes, such as

increasing critical metals investment, expansion of strategic

reserves and loosening policy constrains (for example on nuclear

plants). By investing in high quality opportunities, we aim to

deliver attractive returns over the long run with our mining and

energy investment portfolios. We are also excited in the

business transition of our largest investment, MGX, from an iron

ore producer to a gold developer via the recent acquisition of

the 50% interest in the Central Tanami Gold Project Joint

Venture, which could unlock value by advancing the project with

2.8 million ounces high grade gold resources.

|